Recovering PET waste: A force to foster Cambodia’s rPET sector

-

-

Devi Andriyanti

-

December 8, 2023

-

6 min read

Devi Andriyanti

December 8, 2023

6 min read

Cambodia is dubbed one of Southeast Asia’s fastest-growing economies, with 5.8% GDP growth projected in 2023 by the International Monetary Fund (IMF). Rapid economic growth leads to increased consumption, which also means more waste generation.

As per available data from Phnom Penh, Polyethylene terephthalate (PET) from PET bottles and PET cups ranks second (following plastic bags) in the recyclables waste types generated.1 As the economy and consumption continue to grow, the volume of PET waste is expected to increase in tandem.

PET waste has not received as much attention as plastic bag waste in Cambodia; however, rising demand for recycled PET (rPET), a growing PET recycling industry in other Southeast Asian countries, and Cambodia’s inability to export plastic waste to its neighboring countries due to import bans all provide tailwinds for the development of the PET waste recycling sector in Cambodia.

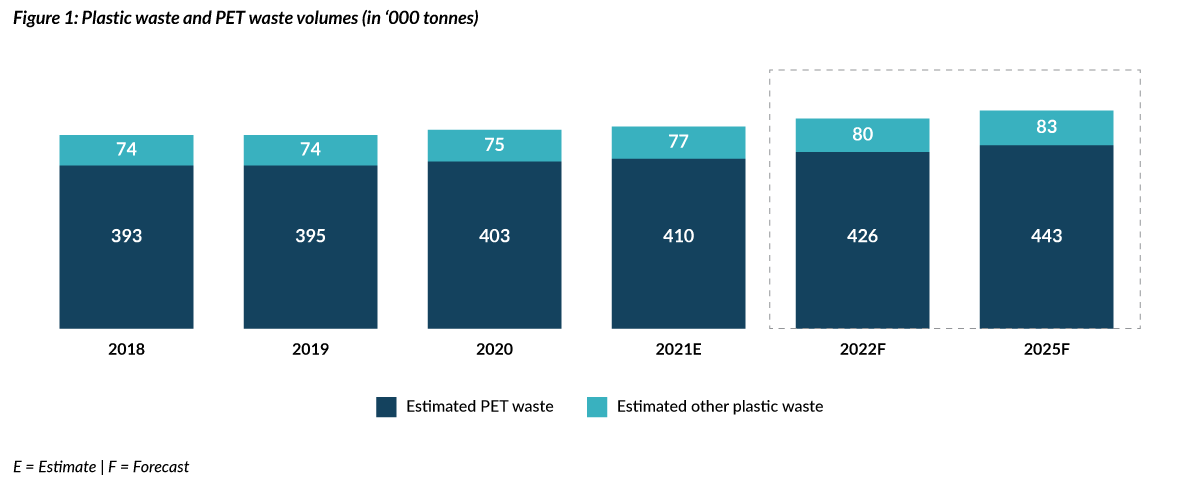

There is little to no data on the volume of PET waste generated in the country; however, Municipal Solid Waste (MSW) data provides a useful guide to estimate the market potential.2 The Circulate Initiative has estimated that approximately 75,000 tonnes of PET waste was generated in 2020. This estimate is based on the assumption that 10% of MSW generated in Cambodia is plastic waste2 and 15.8% of the plastic waste is PET waste, which is based on the average PET share for nine Southeast Asian cities (Jakarta, Makassar, Surabaya, Bangkok, Chon Buri, Rayong, Hanoi, Ho Chi Minh City, and Da Nang) from research conducted by The Circulate Initiative in 2022. Volumes are expected to continue to grow, reaching 83,000 tonnes in 2025 and growing at a compound annual growth rate (CAGR) of 2% between 2023 and 2025 (see Figure 1).

Investments required to grow Cambodia’s recycling sector

PET waste is projected to increase; however, Cambodia’s current waste management and recycling infrastructure is not set up to handle the waste generated. Source segregation is limited, waste collection services are mostly confined to the main cities, and no large-scale waste treatment or recycling facilities exist.2

In 2021, Cambodia’s Ministry of Environment estimated that approximately US$110 million would be needed to purchase the necessary equipment for optimum waste collection in all cities and districts. This estimate, however, does not include the financing needed to build recycling plants.2

Private investment in Cambodia’s waste management and recycling sectors has also been minimal. The Plastics Circularity Investment Tracker reveals that only four private plastics circularity3 deals took place in Cambodia between January 2018 and June 2023, with a total deal value of less than US$50,000 (deals with disclosed value only). Likewise, there are only a few noticeable waste management and recycling players in the country; for example, CINTRI and Global Action for Environment Awareness (GAEA) for waste management and GOMI Recycle 110 in recycling.

As identified by the United Nations Development Programme (UNDP) in 2022, recycling projects are investment opportunity areas that have the potential for high development impact and growth in Cambodia. However, the economics of recycling face a number of constraints in Cambodia, and returns are currently difficult to achieve for large-scale waste recycling projects. The insufficient supply of clean, good-quality feedstock is a key barrier to driving further investment in recycling. Relevant support through various policy initiatives and strong implementation can help to overcome the challenge in Cambodia’s PET waste recovery.

Robust regulation and policy support are needed to grow private investment

In 2015, Cambodia developed Sub-Decree No. 113, which covers the sorting and management of MSW and outlines penalties for non-compliance. However, implementation has not been stringent as the waste collected is still mixed. To make this sub-decree more effective, the government can further encourage awareness through education in schools and in households and provide the required equipment and proper infrastructure management for segregation, such as a set of labeled, colored bins for residents to separate their waste and scheduling trucks to collect one category of waste at a time. Analysis from Delterra’s Rethinking Recycling projects in Indonesia and Argentina shows that source separation of waste is more cost-effective than utilizing waste-sorting technology to process mixed waste, at US$50-US$150 vs. US$200-US$700, respectively for each ton of recyclables per year.4

The introduction of financial incentives is another approach that could enhance the country’s waste management systems. Mexico provides useful guidance in this regard. A price-incentive model from Ecología y Compromiso Empresarial (ECOCE) for informal waste workers was introduced to encourage greater PET bottle collection. Combined with the implementation of waste prevention and management regulations and financial support from various private sources, this model managed to increase Mexico’s rPET feedstock and recycling rates and consequently mobilized the capital to develop local recycling infrastructure.5 Such a mechanism can increase feedstocks, improve the livelihoods of the estimated 3,000 informal waste workers, and potentially incentivize private investment in Cambodia’s recycling businesses.

Both policy support and private investment are required for Cambodia’s waste management and recycling services to keep up with the nation’s plastic waste generation. The government of Cambodia should continue its efforts to create a more conducive environment to attract more private investments by robustly implementing the existing regulations and policies, and introducing new incentivizing ones. On the ground, further waste characterization studies and research on the market potential for a circular economy for plastics in Cambodia will provide the necessary data to allow private investors to make informed decisions and assess relevant investment opportunities.

References

1 Seng, B., Fujiwara, T., and Seng, B. (2018). Suitability assessment for handling methods of municipal solid waste. Global Journal of Environmental Science and Management [online]. Available from: https://doi.org/10.22034/gjesm.2018.04.02.001.

2 Pheakdey, D.V., Quan, N.V., Khanh, T.D., and Xuan, T.D. (2022). Challenges and Priorities of Municipal Solid Waste Management in Cambodia. International Journal of Environmental Research and Public Health [online]. 19(14), 8458. Available from: https://doi.org/10.3390/ijerph19148458.

3 Plastic circularity is defined as a system that drives a circular economy for plastics. This includes technologies, business models or other solutions that tackle the plastic pollution challenge by eliminating, reducing or reusing plastic, or by keeping plastic materials in circulation without them leaking into the environment.

4 Delterra and The Circulate Initiative. Making ‘Cents’ of Recycling Behavior: The Return on Investment of Spreading the Recycling Habit [online]. Available from: https://delterra.org/wp-content/uploads/2022/07/Delterra-TCI-Recycling-Behavior-ROI.pdf.

5 Global Plastic Action Partnership. (2022). Unlocking the Plastics Circular Economy: Case Studies on Investment [online]. Available from: https://www.globalplasticaction.org/resources/case-studies/aJY680000008OLiGAM#.